By Logan Parker September 8, 2025

The various pricing models that processors offer are at the heart of the confusion surrounding one of the most important yet perplexing parts of managing a business: processing payments. Although interchange-plus, flat, and tiered pricing structures all promise savings or ease of use, the truth is much more complex. While the correct model can offer stability and transparency, the incorrect one can subtly reduce margins for retailers.

Understanding how these models operate is even more crucial for businesses in 2025 as new technology, changing regulations, and changing consumer payment trends are introduced. To assist merchants in making more informed decisions that support their objectives and financial performance, this article dissects each strategy and weighs the advantages and disadvantages of each.

Why Pricing Models Matter More in 2025

Businesses have to deal with growing interchange costs, increased regulatory scrutiny, and consumer demand for digital-first transactions as the payments ecosystem develops. There is no longer a one-size-fits-all pricing model. A retail store might require cost predictability, but an online subscription service might place a higher priority on transparency.

Complex fee structures and hidden markups can have a significant impact, particularly on small businesses already struggling with supply chain pressures and inflation. By 2025, merchants will consider the impact of their pricing models on forecasting, scalability, and customer experience, in addition to the amount of processing fees they incur.

As merchants navigate evolving payment solutions in 2025, it’s vital to look past headlines like advertised processing percentages and weigh provider features like transparency, support, and flexibility. A helpful resource on comparing offers beyond just rate explores why evaluating total value—not just the number—can help businesses make smarter, more sustainable choices.

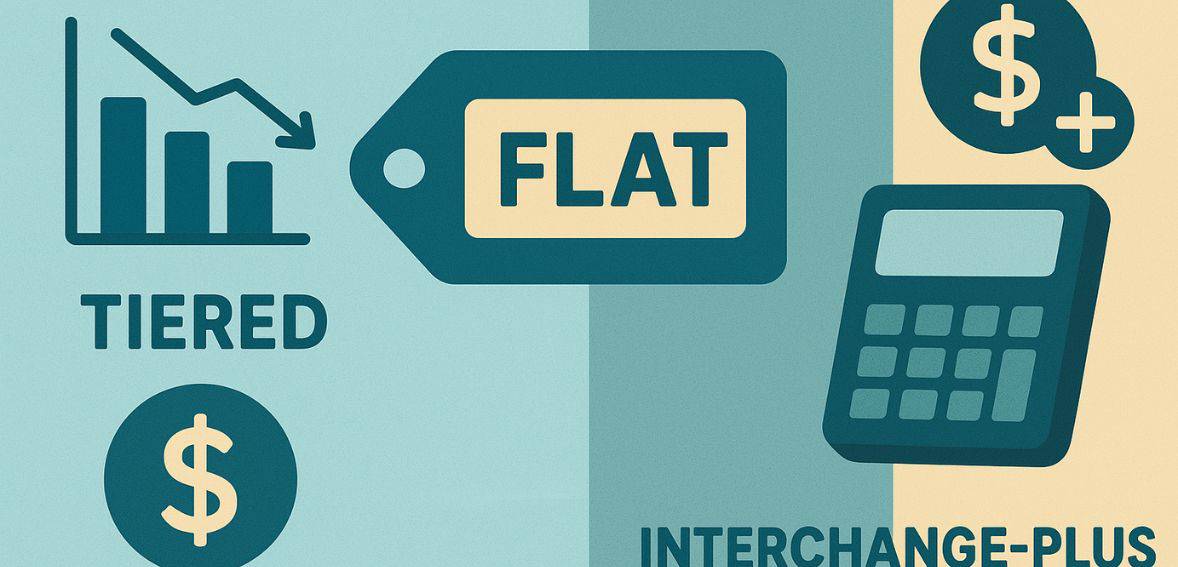

The Basics of Tiered Pricing

Due in large part to processors’ promotion of it as simple, tiered pricing has been one of the most widely used models for years. Three general tiers—qualified, mid-qualified, and non-qualified—are used to classify transactions under this model. Merchants are informed that the majority of transactions will fall into the lower-cost categories, and each tier has its own rate.

But in practice, a lot of transactions wind up in the more costly tiers, which surprises businesses when their effective rate is significantly higher than they had expected. This lack of transparency is ideal for tiered pricing.

Statements frequently lack clarity, and merchants rarely know ahead of time which transactions are eligible for reduced rates. Because it is predictable on paper and well-known in the market, some companies continue to use tiered pricing in spite of these disadvantages.

How Tiered Pricing Impacts Businesses

Unpredictability is the main problem with tiered pricing. A florist, for instance, might believe that the majority of their credit card transactions are eligible for the lowest rates, only to find out that rewards cards or specific debit card transactions move them up into higher tiers. As a result, the blended effective rate is significantly higher than the rate that was advertised.

This unpredictability can become a financial burden for companies with narrow profit margins. As more consumers turn to contactless payments, digital wallets, and premium rewards cards in 2025, tiered pricing frequently penalizes companies for merely taking the most popular payment methods. Over time, a seemingly simple choice frequently becomes one of the priciest.

Hidden Markups in Tiered Pricing

The presence of hidden markups is among the most disregarded features of tiered pricing. Although most transactions fall outside of that tier, processors frequently advertise “qualified” rates that seem appealing.

Digital wallet payments, corporate cards, and premium credit cards are regularly downgraded into higher categories, sometimes without the merchants’ knowledge. These downgrades come with additional, rapidly compounding hidden costs. The problem gets worse by 2025 as more customers use premium rewards cards.

Inflated rates are frequently paid by merchants who are locked into tiered models under the guise of inevitable processing expenses. Businesses are at a severe disadvantage since they are unable to contest or bargain over these markups in the absence of transparency.

The Basics of Flat-Rate Pricing

Because of companies like Square, Stripe, and PayPal, flat-rate pricing has become more and more popular. Regardless of the kind of card or payment method used, businesses pay a single flat rate for all transactions under this model. Because of its simplicity, it appeals greatly to startups, small enterprises, and lone proprietors who do not wish to decipher complex statements.

The flat fee is typically stated as a percentage plus a set amount per transaction, such as 2.9% + $0.30. The benefit is predictability, even though this might appear more expensive than a qualified tier rate. Financial planning and budgeting are made easier for merchants because they are aware of the exact amount they pay for each transaction.

The Pros and Cons of Flat-Rate Pricing

The simplicity of flat-rate pricing is its biggest benefit, but this convenience often comes at a cost. Businesses frequently pay more because processors build in a margin above interchange, making it essential to weigh the flat-rate credit card processing pros and cons before deciding if simplicity outweighs long-term savings.

This adds up to a substantial amount for merchants with high volume. Flat-rate pricing is most appropriate for companies with low transaction volumes, erratic sales patterns, or those that prioritize convenience over cost savings in 2025, as interchange-plus and other transparent pricing models become more widely available. It gets harder to overlook the cost difference for growing businesses.

Why Flat-Rate Works for Micro-Merchants

For micro-merchants and small startups, flat-rate pricing is still a lifeline despite its higher cost structure. The simplicity greatly surpasses the possible savings of more complicated models for a home-based business handling only a few dozen transactions per month or a lone artisan selling at weekend markets. Usually, these retailers don’t have the volume or bargaining power to take advantage of interchange-plus arrangements.

Furthermore, when every dollar counts, the fixed cost of flat-rate pricing offers comfort. The appeal of flat-rate models is further supported in 2025 by the widespread use of mobile point-of-sale systems, app-based sales, and e-commerce side projects. Instead of worrying about figuring out complicated monthly statements, they let new business owners concentrate on expanding their enterprise.

The Basics of Interchange-Plus Pricing

Most people agree that the most transparent pricing model is interchange-plus pricing, also known as cost-plus pricing. In this case, the processor charges the precise interchange fee determined by card networks in addition to a tiny markup that is revealed to the retailer. Interchange-plus offers line-item detail for every kind of transaction, in contrast to tiered pricing, which bundles costs into nebulous categories.

Because of this transparency, merchants can see exactly where their money is going and which part goes to the processor and which to the card networks. As companies seek more accountability in 2025, interchange-plus is fast emerging as the model of choice for those who value cost containment and financial transparency.

Why Interchange-Plus Appeals to Growing Businesses

Interchange-plus’s biggest benefit is that it grows with the business. By negotiating reduced markups, a retail chain that processes millions of dollars a year can make sure they aren’t overpaying as it’s volume increases. Additionally, transparency increases trust because it lets merchants know they aren’t being duped by arbitrary classifications or hidden fees.

However, very small businesses may find this model overwhelming. Statements are more in-depth and can be difficult to understand without some financial knowledge. The additional complexity might seem like more work than it’s worth for startups with constrained bandwidth. However, interchange-plus offers the best balance between cost-effectiveness and equity for mid-sized and large enterprises in 2025.

Interchange-Plus and Negotiation

Negotiating processor markups as volume increases is one of interchange-plus pricing’s most potent features. Small businesses may begin with a small markup, but as transaction volumes increase, they have more influence to demand lower prices. Interchange-plus changes as the business does, in contrast to flat or tiered models that force merchants to accept fixed rates.

Given that astute retailers are aware of their options, more processors will be prepared to compete on markups by 2025. Real savings opportunities are created by this competition, which directly benefits merchants. Interchange-plus is not only transparent but also flexible for long-term expansion when companies routinely review and renegotiate their agreements, which frequently results in significant reductions in overall fees.

Comparing Models in 2025

The differences between tiered, flat, and interchange-plus pricing are evident when comparing them side by side. Although it seems simple, tiered pricing conceals higher costs and unpredictability. Although flat-rate pricing makes budgeting simple, it can be costly for large businesses. Although it takes more work to understand, Interchange-plus offers transparency and fairness.

Businesses that depend on opaque models run a higher risk of overpaying in 2025 as regulatory pressure mounts and card networks continue to modify interchange rates. The size of the company, the volume of transactions, and the degree of financial control a merchant wishes to preserve all play a significant role in making the best decision.

The Effect of Changing Consumer Habits

The way that these models affect businesses in 2025 is also greatly influenced by consumer behavior. Interchange rates are changing as contactless payments, digital wallets, and credit cards with lots of rewards become more popular. Premium cards with higher interchange fees are now preferred by more customers.

Whether they are aware of it or not, this frequently results in higher effective rates for merchants using tiered or flat-rate models. Conversely, interchange-plus merchants are able to view the precise costs associated with every type of transaction. Making an informed choice regarding pricing models requires an understanding of these changing behaviors, particularly as digital-first payments continue to rule the market.

Regulatory Pressures and Transparency Demands

In 2025, there is greater scrutiny than ever before on the payments sector. Regulators are closely monitoring the impact of growing interchange costs on small businesses, as well as hidden fees and a lack of transparency. In this context, there is growing criticism of opaque models such as tiered pricing.

Some processors are adjusting by providing hybrid models or lower markups in response to merchant demands for more transparent disclosures and equitable terms. Companies run the risk of falling behind if they don’t review their pricing strategies in light of these developments. Selecting a model that satisfies regulatory requirements and financial objectives is now required, not optional.

Choosing the Right Model for Your Business

The choice ultimately comes down to priorities. Even though it costs a little more, a neighborhood coffee shop might appreciate the ease of flat-rate pricing. Interchange-plus may end up saving a substantial amount of money for a mid-sized retailer with increasing volume.

In 2025, tiered pricing will have fewer benefits due to the emergence of more transparent alternatives, even though it is still widely used. The secret for any business is to consider a model’s growth plans, transaction volume, and complexity tolerance before accepting it without question. The option that strikes a balance between operational ease and cost savings is the best one.

The Future of Pricing Models Beyond 2025

The payment pricing landscape is probably going to keep changing in the future. Predictability and transparency are already being combined in hybrid models that give merchants the best of both worlds. Automation and artificial intelligence might also be involved, assisting companies in examining transaction data and locating undiscovered cost savings possibilities.

There is no doubt that passive merchants will keep overpaying. It will continue to be crucial to stay informed, ask the right questions, and routinely review processing agreements. The 2025 models are only one phase of the payments industry’s continuous transformation.

Conclusion

The important takeaway for 2025 is that no company can afford to overlook the differences between tiered, flat, and interchange-plus pricing, each of which has advantages and disadvantages. Transparency and control are more important than ever in a time of changing consumer payment preferences, increasing interchange rates, and increased regulatory scrutiny.

In addition to cutting expenses, merchants who take the time to comprehend these models and make informed decisions will increase their financial stability. Making the correct decision can mean the difference between paying hidden premiums and creating a sustainable future, regardless of whether you prefer the simplicity of a flat-rate or the equity of interchange-plus, or the waning familiarity of tiered pricing.